Overview

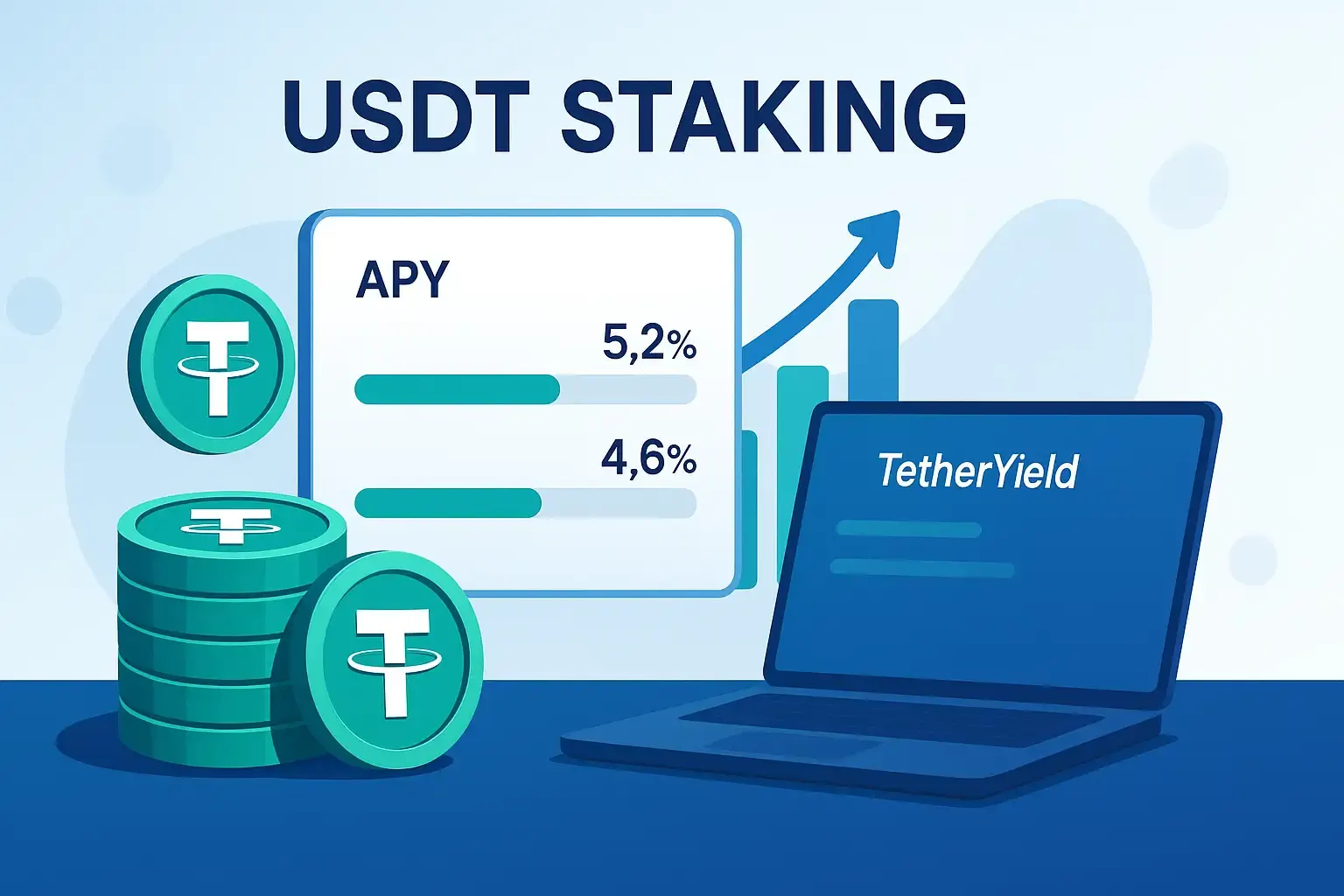

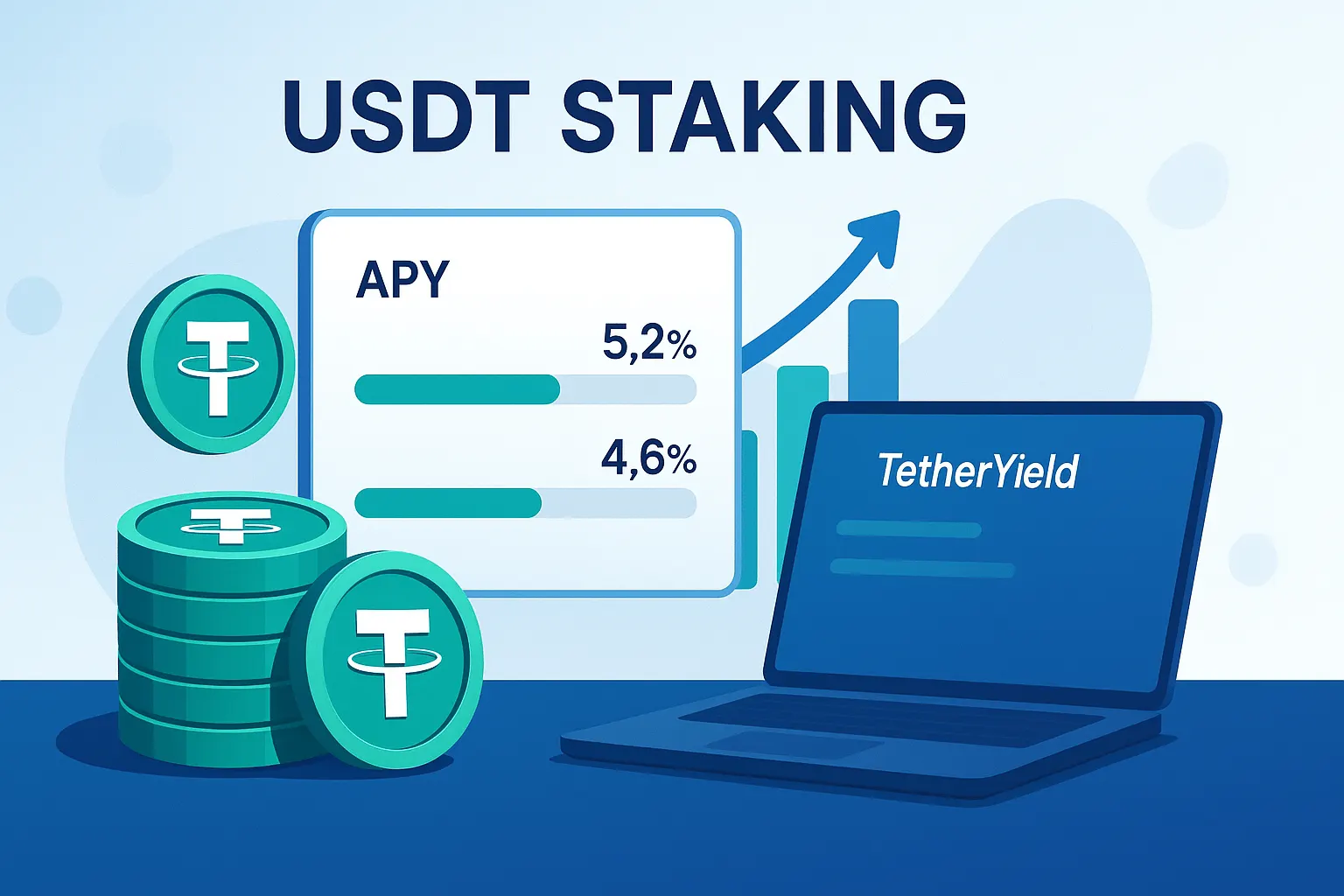

USDT staking – the practice of earning interest or rewards by locking up Tether (USDT) stablecoins – has surged in popularity as crypto investors seek low-risk ways to grow their holdings. Stablecoins like USDT have exploded in use, reaching a total market cap of over $300 billion in 2025 with Tether alone commanding roughly 59% of the market (about $183 billion in circulation). This massive adoption underscores how USDT has become a cornerstone of the crypto ecosystem, not just for trading but also as a tool for passive income generation. Investors are increasingly looking to stake USDT to earn steady yields that far exceed traditional bank interest rates, all while avoiding the wild price swings of other cryptocurrencies. USDT staking dashboard showing high APY yields on TetherYield Stablecoins like USDT have seen remarkable growth by 2025, with Tether’s market cap (green) reaching $183B and dominating ~59% of the sector. This rise in stablecoin usage fuels the demand for USDT staking as a passive income strategy.In this comprehensive guide, we’ll explore what USDT staking is, how it works, and why it’s so appealing for both crypto newcomers and seasoned investors. We’ll compare different staking options – from centralized exchanges to DeFi protocols – and highlight the top platforms for staking USDT in 2025. You’ll also learn about the benefits, potential risks, and how a specialized service like TetherYield.com can offer industry-leading returns on your USDT. Whether you’re looking to earn interest on idle stablecoins or maximize yield on your digital dollars, this article will equip you with the expert knowledge to make informed decisions. Let’s dive into the world of USDT staking and discover how to turn stablecoins into a high-yield passive income stream.What Is USDT Staking?USDT staking refers to the process of depositing your Tether (USDT) stablecoins into a platform or protocol to earn rewards over time. Unlike traditional crypto staking (which involves locking up coins to secure a proof-of-stake blockchain), staking USDT does not help validate any network. Instead, your USDT is typically lent out to borrowers or provided as liquidity in exchanges, and you earn interest or a share of fees in return. In simpler terms, staking USDT is akin to putting your dollars in a high-yield savings account – but one powered by crypto markets rather than a bank.Tether (USDT) is a stablecoin pegged 1:1 to the U.S. dollar, which means its value remains around $1.00. By staking USDT, you can generate income from an asset that maintains a stable value, avoiding the volatility risk of coins like BTC or ETH. This stability makes USDT an attractive option for earning yield without exposing your principal to large price swings. In fact, USDT’s dominance and liquidity (over 93 million holders as of late 2025) ensure it’s widely accepted across platforms, giving stakers plenty of choice where to earn rewards.How USDT staking works: When you stake (or deposit) USDT on a platform – be it a centralized exchange or a decentralized finance (DeFi) protocol – the platform will put your USDT to work. Commonly, deposited USDT is:

Lent out to margin traders or borrowers who pay interest.

Supplied to liquidity pools on decentralized exchanges, earning a share of trading fees.

Used in yield farming strategies or incentive programs that offer rewards.

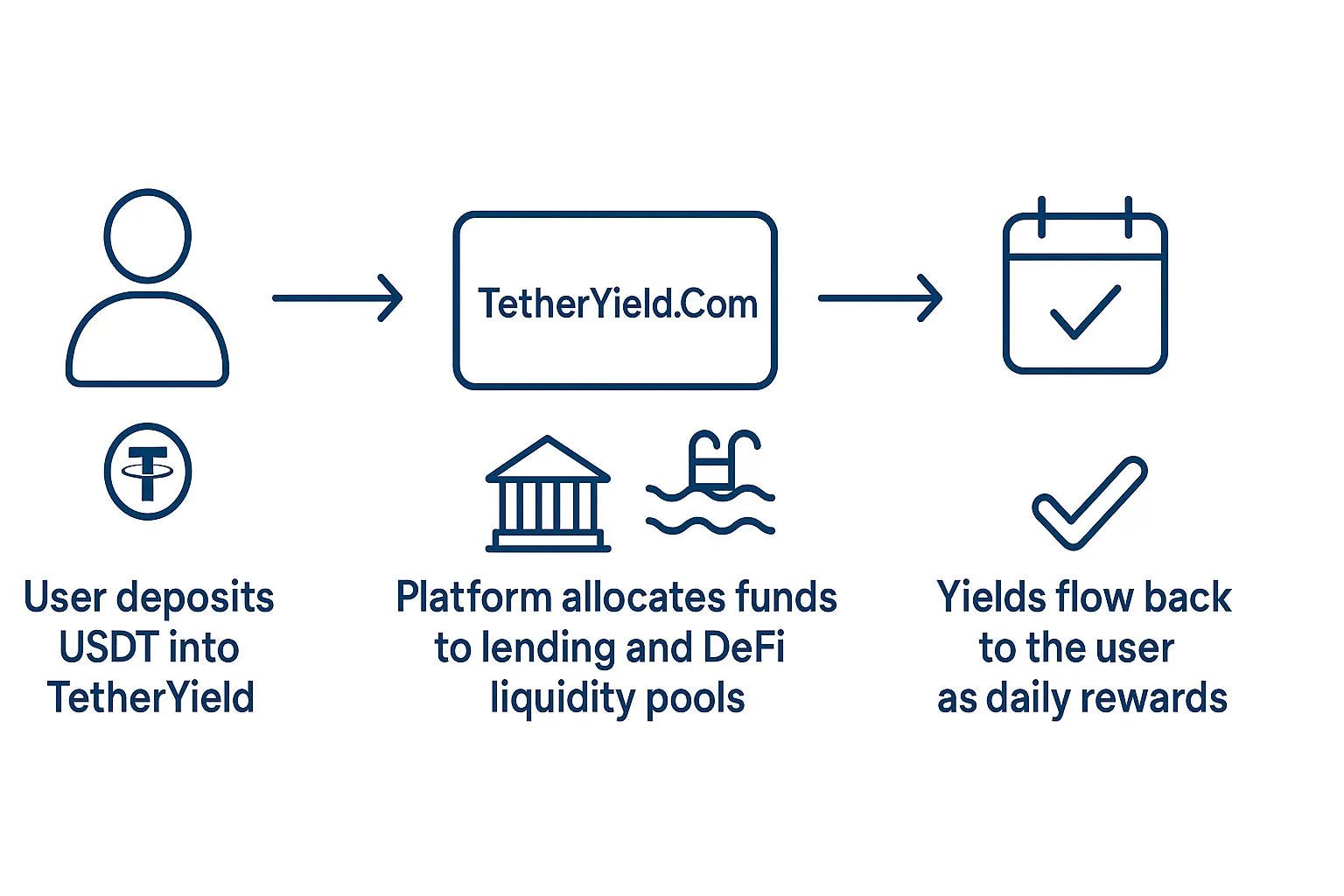

Because of this activity, the platform can pay you a yield, usually quoted as an Annual Percentage Yield (APY). The APY represents how much your USDT could grow over a year, with compounding taken into account if rewards are reinvested. (By contrast, an APR is a simple annual rate without compounding.) For instance, a 10% APY means $1,000 in USDT would become about $1,100 after one year, assuming earnings are continually reinvested. Many crypto platforms advertise APY since it appears higher due to compounding effects – always check whether a quoted rate is APY or APR when comparing opportunities.It’s important to note that when staking USDT, you remain the owner of your stablecoins, and you can typically withdraw your funds (plus earned interest) after a certain period or even anytime, depending on the platform’s rules. In summary, USDT staking is essentially earning interest on your digital dollars by allowing them to be used in the crypto markets’ lending and trading infrastructure.Infographic explaining how USDT staking on TetherYield works from deposit to daily rewardsHow Does USDT Staking Work?The process of staking USDT can be broken down into a few simple steps, regardless of which platform or method you choose:

Deposit USDT: You transfer your USDT tokens to the platform or smart contract. For centralized services (CeFi), this may involve sending USDT to your account on an exchange or app. For DeFi, you connect your crypto wallet and approve the smart contract to use your USDT.

Allocation of Funds: The platform then allocates your USDT to a yield-generating activity. In CeFi, that might be issuing an over-collateralized loan to a vetted borrower or allocating to an institutional lending desk. In DeFi, it could mean your USDT goes into a lending pool (like Aave or Compound) or a liquidity pool on a DEX, where it helps facilitate trades. Some advanced platforms run automated strategies behind the scenes to optimize returns, possibly moving funds between different protocols.

Interest Generation: As your USDT is utilized, it earns yield. Borrowers pay interest on loans, traders pay fees to liquidity pools, and some protocols may offer bonus tokens as incentives. All these forms of compensation accumulate as earnings. The yield can be fixed (a set rate) or variable (fluctuating with market demand). Many platforms update the earned interest daily or in real-time.

Payout to You: The rewards are distributed to you as the lender/staker. Depending on the platform, this could happen daily, weekly, or upon unstaking. Some platforms pay in USDT itself (making compounding easy if you leave it staked), while others might reward you in a different token. For example, a DeFi protocol might give you their native token on top of interest. If there’s a lock-up period, you’ll get your principal back at the end of the term along with any accrued interest. On flexible terms, you can withdraw your USDT and earned interest whenever you like, giving you liquidity if you need it.

It’s worth reiterating that USDT staking is not mining or traditional staking – you’re not helping create new blocks or new USDT. Instead, your yield comes from real economic activities like lending and trading fees. This is why stablecoin staking returns are often more modest than the triple-digit APYs sometimes seen in meme coin staking; the yields are tied to things like interest paid by borrowers or exchange fee revenue, which have more stable, sustainable ranges. However, during certain periods or with incentive programs, yields on USDT can spike higher due to promotions or high demand for liquidity.Let’s illustrate with a quick example: Suppose you stake $10,000 USDT on a platform offering 8% APY. Behind the scenes, your USDT might be lent out via a DeFi lending pool where borrowers pay, say, 10% interest. The platform takes a small cut (maybe 2%) and gives you 8%. Over a year, your $10k would generate about $800 in interest (if the rate stays constant). If the interest is paid daily and compounded, you’d actually earn slightly more – that’s the APY effect. Some platforms also have mechanisms to auto-reinvest your earnings to maximize compounding.In summary, staking USDT works much like a decentralized savings account: you deposit stablecoins, they’re put to productive use in the crypto markets, and you receive interest. The key differences from a bank are the typically higher yields and the different risk profile (which we’ll discuss later). With the mechanics explained, let’s move on to why so many investors are excited about USDT staking in the first place.Why Stake USDT? The Benefits of Staking TetherStaking USDT offers several compelling benefits that make it an attractive strategy, especially for those who value stability in their investments. Here are the key advantages of staking USDT:

Passive Income on Stable Assets: The primary benefit is earning passive income on an asset that remains pegged to $1.00. Unlike volatile cryptocurrencies, USDT won’t suddenly drop in value 20% overnight. This means your principal is protected from market swings while it earns interest. Investors can enjoy steady returns without the stress of price volatility. It’s an appealing proposition: your money works for you, and you don’t have to constantly monitor the market.

Higher Yields than Traditional Banks: USDT staking yields are typically far superior to what you’d get with a regular bank account or even many traditional investments. For example, in late 2025 the average U.S. savings account rate was around a measly 0.40% APY, and even the best high-yield savings accounts offered roughly 4–5% APY. By contrast, reputable crypto platforms often provide stablecoin APYs in the mid to high single digits, and some even higher. U.S. Treasury Series I savings bonds were yielding ~3.98% in mid-2025 – still below many USDT staking rates. This significant yield differential makes staking USDT a compelling alternative for those seeking better returns on cash holdings. Essentially, you can beat inflation and bank rates by putting your dollars into USDT and staking them in crypto markets.

Reduced Risk vs. Volatile Crypto Investing: Staking USDT can be seen as a lower-risk strategy in the crypto world. Because USDT is a stablecoin, you avoid the large price swings associated with coins like Bitcoin or Ethereum. In a turbulent market, holding stablecoins is a way to preserve capital. Staking them adds the benefit of growing that capital. It’s a popular strategy for investors who have taken profits from other coins and want to park funds in a stable asset that still yields a return. In 2025, with Bitcoin hitting new highs then experiencing corrections, many found refuge in stablecoin yields as a way to hedge against volatility while still participating in the crypto ecosystem.

Liquidity and Flexibility: Many USDT staking options offer flexible terms, meaning you can withdraw your funds at any time without penalty. This is especially true on platforms with “flexible savings” or DeFi protocols – you’re not locked in, so your money remains fairly liquid. Even some fixed-term products have relatively short durations (e.g. 30, 60, or 90 days). Compared to a traditional bank CD or bond that might lock your funds for years, stablecoin staking can give you more agility. Additionally, USDT’s wide acceptance means you can quickly convert it to cash or other crypto if needed, giving stakers peace of mind that their funds aren’t tied up indefinitely.

Ease of Use & Accessibility: These days, staking USDT has become user-friendly. Major exchanges and platforms offer simple interfaces – often just a few clicks to subscribe your USDT to a savings or staking program. There’s no need for advanced technical knowledge, especially with centralized providers. Even in DeFi, interfaces have improved, and some wallets make it as easy as using a banking app. Furthermore, the entry barrier is low – you typically can start with as little as $10 or $100 worth of USDT. This democratizes access to high yields, allowing even small holders to earn interest on their stablecoins. In fact, on TetherYield the minimum to start is just $10 USDT to begin earning daily profits.

Compounding Returns: Many platforms pay out rewards regularly (daily or weekly) and allow you to automatically reinvest them. This means your earnings start earning more earnings – the magic of compounding. Over time, compounding can significantly boost your total returns. For example, an 8% APY compounded daily yields more than 8% simple interest. Staking makes it easy to continually roll over your rewards into the principal. If you’re patient, this can snowball your passive income.

Diversification and Stable Hedge: Staking USDT can play an important role in a balanced crypto portfolio. It provides a stable counterweight to high-risk, high-reward investments. During bull runs you might convert volatile gains into USDT to lock in profits, and staking those USDT ensures they’re not just sitting idle. During bear markets, staking stablecoins gives you a yield to offset some losses elsewhere and maintain cash flow. It’s a strategy that combines capital preservation with income generation, which is rare in the crypto space. As noted by industry analyses, stablecoin staking has evolved from a niche tactic to an “essential financial instrument” by 2025, used to generate reliable yield in a maturing digital economy.

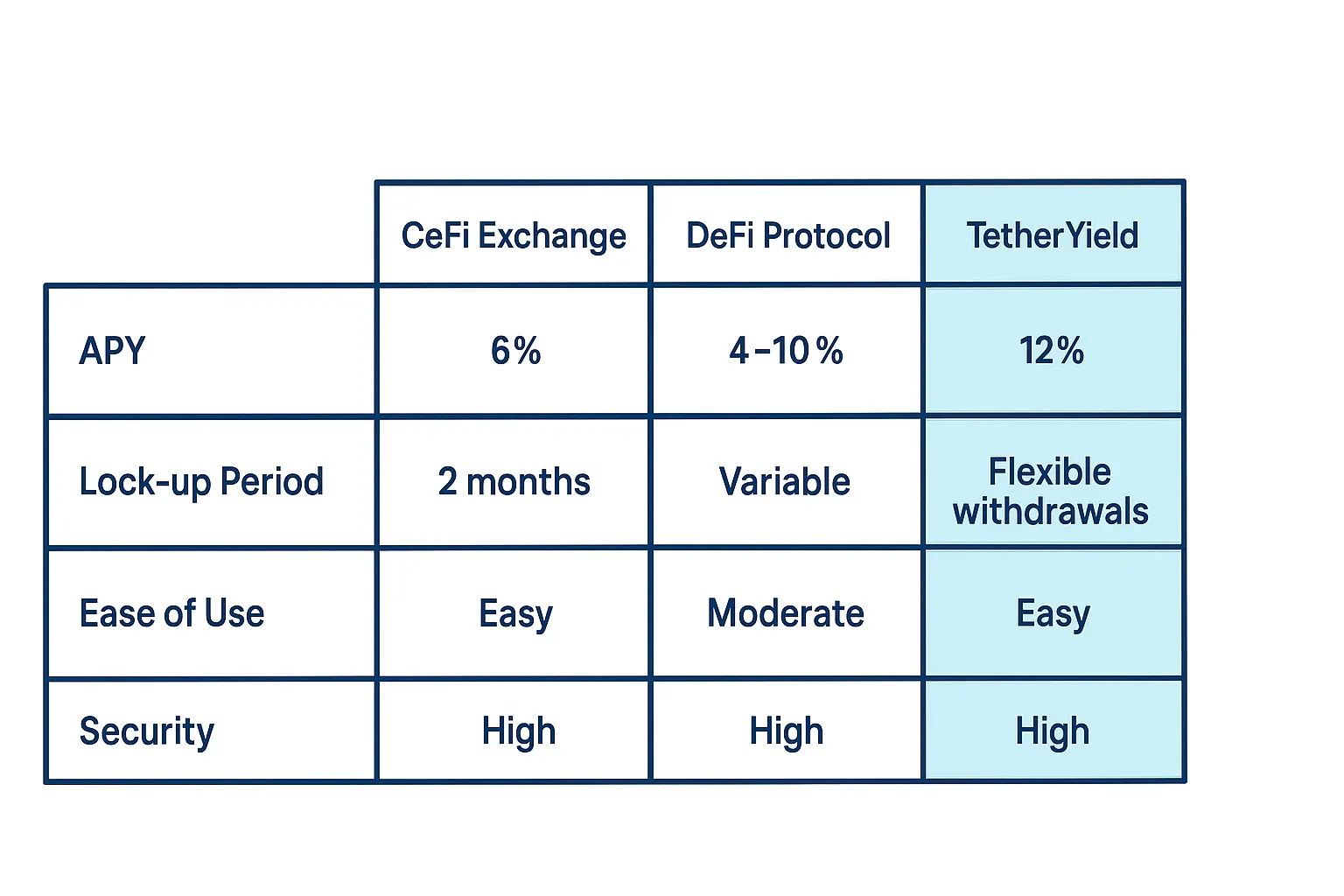

In short, the benefit of staking USDT is enjoying high-yield, low-volatility returns. You get the best of both worlds: the steadiness of the U.S. dollar and the attractive interest rates of the crypto market. That said, these rewards do not come completely free of risk. It’s important to understand the considerations and potential pitfalls before you allocate a large portion of your savings into USDT staking. In the next section, we’ll discuss the risks and how to manage them so you can stake smarter.Comparison chart of USDT staking options on CeFi exchanges, DeFi protocols and TetherYieldRisks and Considerations of USDT StakingWhile staking USDT is generally considered a relatively safe and conservative crypto strategy, it’s not entirely risk-free. Anyone considering staking their Tether should be aware of the following risks and take steps to mitigate them:

Counterparty Risk (Platform Risk): When you use a centralized platform or even some DeFi protocols, you are trusting a counterparty with your funds. In CeFi, this means the exchange or lending company could fail or go bankrupt, potentially putting your deposit at risk. We saw examples in the past (like Celsius or other lending platforms) where users lost funds due to insolvency. Even if funds are insured or the platform has a strong reputation, there’s always a non-zero chance of default or fraud. In DeFi, counterparty risk is replaced by smart contract risk, but more on that shortly. To manage this risk, stick to reputable platforms with transparent operations, audits, and ideally insurance coverage or collateralization of loans. Platforms like TetherYield, for instance, bolster confidence by maintaining SOC 2 and ISO/IEC 27001:2022 certifications and insuring assets via a top insurer (Lockton) – these are signs of a serious commitment to security and accountability.

Smart Contract Vulnerabilities: In decentralized protocols (and even some centralized ones that deploy on-chain contracts), bugs or exploits in the code can lead to losses. For example, a flaw in a lending pool’s smart contract could be exploited by hackers, causing funds to be drained. These technical risks are not easy for the average user to assess. However, using platforms that undergo independent security audits by reputable firms (like CertiK, Quantstamp, etc.) can reduce the likelihood of vulnerabilities. Also, diversifying across different protocols can limit exposure – if one gets hacked, you don’t lose everything.

Liquidity and Lock-up Risk: Some USDT staking offers (especially those with very high yields) might require you to lock your funds for a fixed term (30 days, 90 days, or more). During that lock period, you generally cannot withdraw your USDT without penalty. This creates risk if you suddenly need funds for an emergency, or if market conditions change and you want to reallocate. There’s also the scenario of a major market event – if a platform halts withdrawals (we saw this in some crises), you may be stuck. To mitigate this, consider keeping a portion of your capital in flexible staking options or simply as liquid USDT that isn’t staked, as an emergency buffer. Also, pay attention to the terms: some platforms like TetherYield advertise “instant and on-demand withdrawals” with no lock-up, which significantly lowers liquidity risk for users.

Stablecoin Depeg Risk: USDT is designed to always equal $1, but in extreme circumstances a stablecoin can lose its peg (trade below $1) due to panic or solvency concerns. Tether has historically maintained its peg well, but there have been brief moments where it traded at $0.97-$0.98 during market stress. More dramatically, algorithmic stablecoins have collapsed in the past (though USDT is fully reserve-backed, not algorithmic). The risk for USDT is if there were ever a serious doubt about Tether’s reserves or a regulatory action freezing assets, it could depeg. This would directly reduce the value of your staked USDT. The probability seems low for major stablecoins, but it’s not zero. As a staker, you should keep an eye on news regarding Tether’s reserve attestations and regulatory environment. Some investors mitigate stablecoin risk by diversifying across a few stablecoins (e.g. USDC, DAI) – however, note that yields on different stablecoins can vary and not all platforms support all types.

Interest Rate Fluctuations: If you choose a variable-rate staking product (common in DeFi), the APY can change over time. If a bunch of new people deposit USDT into the same pool, the yield might drop due to supply-demand shift. Or if borrowing demand spikes, yields might go up. Be prepared for yield volatility. Today it might be 10%, next month 5%. On the flip side, if you lock in a fixed rate, you might miss out if rates rise elsewhere. Regularly monitoring your earning rate and being ready to move funds to better opportunities is part of active yield management.

Regulatory and Legal Risk: The regulatory landscape for stablecoins and crypto lending is evolving rapidly. Governments are paying close attention to interest-bearing crypto accounts (some have even labeled certain offerings as securities). New rules could affect your ability to earn yield or the obligations of platforms. For example, in some regions, platforms have had to shut down interest products for retail users or implement strict KYC. In the EU, the MiCA regulation (Markets in Crypto-Assets) is introducing restrictions – such as a ban on stablecoin issuers themselves paying interest directly on tokens – meaning yields must come from external sources like lending or DeFi. These rules aim to make stablecoin services safer (preventing unbacked yield schemes), but they could also limit certain offerings. On a positive note, clear regulations can legitimize the space and encourage institutions to participate, potentially increasing options for users. It’s wise to stay informed about the laws in your jurisdiction. Use platforms that are compliant and transparent about how they generate yield. In the US, for instance, momentum with acts like the proposed Stablecoin Act of 2025 and the GENIUS Act is creating a framework that might allow stablecoin interest under oversight, which could actually expand opportunities in a regulated way.Institutional-grade security protecting USDT staking funds on TetherYield

To sum up, stake with your eyes open. The good news is that many of these risks can be mitigated with due diligence and prudent choices:

Stick to platforms with strong security track records, audits, and insurance if available.

Diversify your stablecoin holdings and staking platforms to avoid single points of failure.

Prefer platforms that prioritize compliance and transparency, as they are more likely to be long-term players in the industry.

Don’t lock all your funds for long durations; keep some accessible.

Monitor the health of the stablecoin itself (Tether’s reserve reports, etc.) and broader market conditions.

If you do the above, staking USDT can remain a very rewarding low-volatility strategy with manageable risk. Now, let’s explore where and how you can stake USDT – the types of platforms available, and which might be the best fit for you.Chart comparing holding USDT versus staking USDT on TetherYield over 12 monthsWhere to Stake USDT: CeFi vs. DeFi OptionsWhen it comes to staking USDT, you have two broad categories of platforms:

Centralized (CeFi) services and Decentralized (DeFi) protocols. Each has its pros and cons in terms of ease of use, yield, and risk. Additionally, there are emerging “hybrid” platforms that try to blend the best of both worlds. Let’s break down your options:Centralized Platforms (CeFi)CeFi platforms include major crypto exchanges and lending services (e.g., Binance, Kraken, Nexo, Coinbase, etc.) that offer interest on deposits. Using these is very straightforward – you usually just transfer USDT to your account and opt into a savings or staking program.Advantages:

User-Friendly: CeFi platforms have polished interfaces and handle all the complexity for you. No need to manage private keys or interact with smart contracts.

Custodial Safety Nets: These platforms often have security measures like insurance funds or FDIC-insured custodial accounts (in the case of some U.S. firms for USD balances). Some, like Kraken, are regulated and comply with strict security standards.

Promotional Rates: Big exchanges sometimes run promotions on USDT staking, boosting yields for a time. They also offer both flexible staking (withdraw anytime) and fixed-term options for higher rates.

No Web3 Hassles: You won’t pay gas fees or worry about blockchain transaction complexities.

Disadvantages

Counterparty Risk: As discussed, you’re trusting the company with your funds. If they mismanage funds or get hacked, you could lose money. Insurance is not guaranteed unless explicitly stated.

KYC Requirements: CeFi will require identity verification. Not everyone is comfortable with that or may not have access if the service isn’t available in their country.

Yield Might Be Lower: Because the platform might take a cut or has higher overhead, the interest rates can be a bit lower compared to raw DeFi. CeFi yields for stablecoins typically range around 2% to 6% APY in normal conditions, though some push higher via special offers.

An example CeFi offering: Binance Earn might give around 5% APY on flexible USDT savings, but occasionally runs promotions up to say 10% for a 30-day lock on USDT. Another example, Nexo, advertises rates up to 16% APR on USDT if you lock for 3 months and hold their token (base rate around 9% otherwise). These are attractive, but often come with conditions (like receiving interest in a platform’s token or holding a membership token). Kraken, known for its security, has offered up to ~4-6% APY on flexible USDT staking and even higher (20%+) on certain fixed terms, likely as promotional or limited-time rates.Overall, CeFi is great for beginners and those who want convenience and a trusted name. Just be sure to choose established platforms and understand any lockup terms.Decentralized Protocols (DeFi)DeFi involves using blockchain-based protocols where you interact directly with smart contracts from your own wallet. Examples include Aave, Compound, Curve, Uniswap liquidity pools, Yearn vaults, and many others that support stablecoins.Advantages:

Higher Potential Yields: DeFi often offers higher interest rates because it cuts out intermediaries. Yields of 3%–10% APY are common, and during incentive programs or high demand, rates can soar well above that. For instance, a yield farm might offer 20%+ on a USDT/ETH liquidity pool including reward tokens.

You Control Your Funds: Funds remain in your personal wallet and are just “locked” in a smart contract. You’re not giving them to a company, so you avoid counterparty risk. You can withdraw (usually) anytime, subject to network conditions.

Transparency: You can see exactly how the smart contract works (if you can read code or trust audited code) and track funds on the blockchain. Interest rates adjust algorithmically based on supply and demand, often in real-time, which is very transparent.

Innovation: DeFi is where new strategies pop up – you can sometimes find creative opportunities (like providing liquidity on a new DEX or using stablecoin yield aggregators) for extra yield.

Disadvantages

Complexity: Using DeFi requires understanding wallets (e.g., MetaMask), paying gas fees, and knowing your way around DApps. Mistakes (like sending to the wrong address or interacting with a fake contract) can be costly. There’s little recourse if you mess up since there’s no customer support desk on a decentralized protocol.

Smart Contract Risk: As mentioned, there’s a risk of bugs or exploits. Even audited protocols have had issues. There’s no FDIC insurance or lender of last resort – if a hack happens, funds can be irrecoverable.

Variable Rates: The yield can change rapidly. Also, if you’re providing liquidity in a trading pair (like USDT/USDC pool), you might face impermanent loss (though for 1:1 pegged pairs like USDT/USDC it’s minimal).

Fees: On networks like Ethereum, gas fees can eat into your earnings if you’re not deploying a large amount. However, many stablecoin yields are now on cheaper chains or Layer-2 networks, which helps.

A straightforward DeFi example: deposit USDT into Aave on Polygon or Ethereum. You’ll get a variable APY (let’s say 4% at the moment) paid in USDT. If Aave has liquidity mining, you might also receive AAVE tokens boosting the effective APY. Alternatively, provide USDT/USDC to Curve Finance, earning trading fees + CRV incentives, which could total perhaps 5–8% APY, depending on the week. These numbers fluctuate but often sit in high single digits.DeFi is ideal for those who are a bit more tech-savvy and want to maximize yields while keeping custody of their coins. It’s also the only route if you want to avoid KYC entirely. But you must do your homework on the protocols you use.Specialized High-Yield Platforms (CeFi–DeFi Hybrid)In recent times, a new category of platforms has emerged that bridge CeFi and DeFi. Their goal is to give users an easy, centralized interface with customer support, while behind the scenes they utilize DeFi strategies to get better yields. Essentially, they curate and automate DeFi for you, often taking a cut for their service.TetherYield.com is a prime example of this model. Platforms like these operate somewhat like a crypto wealth management service focused on stablecoin yield:

They pool user USDT and deploy it across various yield-generating opportunities – possibly across multiple DeFi protocols, liquidity pools, or even CeFi lending – in order to optimize return.

They handle the heavy lifting (monitoring rates, moving funds, compounding returns) which would be cumbersome for an individual user.

Meanwhile, they present a simple interface and often guarantee certain security standards, audits, and insurance to alleviate user concerns about DeFi’s technical risks.

The advantage is you might get higher yields than standard CeFi without the hassle of DIY DeFi. For instance, TetherYield advertises industry-leading APY that can exceed 100% annually by using an “optimized delegation strategy” across different opportunities. In fact, TetherYield’s plans have ranged from ~47% APY up to a staggering ~730% APY for certain high-risk, high-return tiers. Those numbers are far above typical bank or exchange rates, made possible by actively managing funds in lucrative DeFi ventures and perhaps new project incentives. The platform blends CeFi security (MPC custody, insurance, compliance) with DeFi profits, aiming to give users the best of both.The disadvantage could be that you still face some platform risk (you are trusting the service to manage funds wisely and not get hacked). However, a credible hybrid will be transparent about their strategy and safeguards. They often undergo audits on their smart contract integrations and maintain capital reserves or insurance policies.This category is great for investors who want higher yields but don’t have the time or knowledge to chase them in DeFi themselves. It’s a “have your cake and eat it too” approach: hands-off for the user, but potentially big returns.Bottom line: You can stake USDT in various ways – via CeFi for ease, DeFi for control and potentially higher rates, or through specialized services that combine elements of both. Your choice depends on your comfort with technology, risk tolerance, and yield goals. Many people diversify: for example, put some USDT in a trusted CeFi exchange for ~5%, some in DeFi pools that might net ~10%, and some in an innovative platform like TetherYield aiming for 50%+.Next, let’s look specifically at some of the top platforms to stake USDT in 2025 and what they offer, so you have concrete options to consider.Top Platforms to Stake USDT in 2025Given the numerous choices available, it helps to know which platforms stand out for USDT staking. Below we highlight five of the top platforms for staking USDT as of 2025, each with its unique strengths: Top 5 Platforms to Stake USDT in 2025 – from specialized services to major exchanges. These platforms lead the market by offering attractive yields, security, and ease of use for stablecoin investors.

TetherYield.com – High-Yield Specialist: TetherYield has rapidly become a top choice for USDT staking, thanks to its incredibly competitive APY that can reach into the hundreds of percent. This dedicated platform focuses solely on USDT yield optimization. Users can access APYs ranging from around 47% up to over 800% on certain plans – rates unheard of on regular exchanges. Uniquely, TetherYield supports instant deposits and withdrawals with no lengthy lock-ups, providing liquidity alongside jaw-dropping returns. The platform’s transparent reward structure ensures you see exactly how your daily profits are calculated, and it has built a strong reputation for timely payouts. Security is also a selling point: TetherYield employs institutional-grade security (including multi-party computation for private keys, and full insurance coverage for assets) to protect users’ funds. For anyone serious about maximizing passive income from USDT, TetherYield stands out as a premier option – it combines extremely high yields with a user-friendly experience and robust trust measures.

Binance Earn – Big Exchange Convenience: Binance, one of the world’s largest exchanges, offers a variety of USDT staking products under its Binance Earn umbrella. You’ll find both flexible savings (with rates that fluctuate, often in the ~5% APY range) and fixed-term staking (for example, 30, 60, 90-day) which occasionally come with promotional APYs that are quite attractive. Binance’s strengths are its scale and security – it has a proven track record and extensive security infrastructure (cold storage, SAFU insurance fund, etc.). The sheer number of users and high liquidity on Binance also means redemption or trading of USDT is seamless. It’s worth watching Binance’s events; sometimes they might offer double-digit APY on USDT for a limited subscription period. Additionally, because Binance supports so many assets, you have the convenience of managing all your crypto in one place. The platform provides peace of mind along with earnings, making it a solid choice for those who already trade on Binance and want to put idle USDT to work.

OKX (OKEx) – Exchange with DeFi Integration: OKX is another major crypto exchange that has been gaining traction. It provides USDT staking through its Earn section and often integrates DeFi yields for its users. Select USDT staking pools on OKX have been known to offer APYs as high as ~38% during special events, which is significantly above typical market rates. These opportunities may come and go, but it shows OKX’s commitment to remaining competitive on yields. The platform also touts strong security measures (such as cold storage of funds, multi-factor authentication) and is considered to have institutional-grade safety. With OKX, you also get an all-in-one ecosystem: you can stake, trade, and even explore their integrated DeFi hub (allowing access to on-chain lending pools) from the same interface. This makes OKX an appealing choice for users who want a balance of yield potential and reputable exchange security.

MEXC Global – Flexible and Accessible: MEXC is a crypto exchange known for its user-friendly approach, and it positions itself as a gateway for earning on stablecoins. For USDT, MEXC offers a Flexible Savings product with yields up to about 8.8% APY. The notable thing about MEXC is that even small holders can stake – there’s a low minimum, and interest is typically paid out daily. They also allow withdrawal at any time with no penalties, which is great for flexibility. While 8% may not sound as high as some others on this list, it’s quite competitive for a no-lock, low-hassle product. MEXC’s focus is on accessibility: even if you only have, say, $100 of USDT, you can start earning interest easily. For beginners or those who prioritize liquidity, MEXC is a strong option. Its interface is straightforward and the platform has a decent security track record, making USDT staking simple and safe for the average user.

Kraken – Regulated and Reliable: Kraken is one of the longest-running crypto exchanges and is highly regarded for its compliance and security-first mindset. It offers USDT staking (sometimes termed “Earn” or “Staking” on their platform) with both flexible options and term deposits. Kraken’s rates for USDT have been competitive; at times they have offered up to ~24% APY on certain fixed-term staking, paid out twice monthly. These higher rates can depend on specific programs or regional offerings, but even the baseline rates are attractive given Kraken’s profile. What sets Kraken apart is the confidence it provides to more conservative investors – it has robust financial reserves, has undergone audits, and operates under U.S. regulations (for example, it has a bank charter in Wyoming). Institutional and retail investors alike trust Kraken for its transparency and strong security (they famously have never been hacked in their core exchange). The trade-off is that availability of some staking products might vary by jurisdiction due to Kraken’s compliance with local laws. But if you can access it, Kraken is an ideal choice for those who value safety and legitimacy, yet still want decent yield on their USDT.

These top five cover a spectrum of choices: from a dedicated high-yield service (TetherYield) to large multi-service exchanges (Binance, OKX, Kraken) to a newcomer-friendly platform (MEXC). All of them have something to offer depending on your needs.Of course, there are other places to stake USDT as well – such as Decentralized protocols (Aave, Compound, etc., as discussed earlier) or other CeFi platforms like Nexo, Crypto.com, KuCoin, and more. For instance, Crypto.com might offer around 6-8% on USDT if you lock for 3 months and have their Visa card stake (it was roughly 6.9% on large amounts with conditions). Nexo we mentioned can go up to 16% with conditions. Ledn is another, offering around 6.5–8.5% without token hoops. These can be good alternatives if you already use those services.When choosing, consider the following:

Yield vs. Lock-up: Higher APYs often require locking your USDT for a period or fulfilling certain conditions. If you need flexibility, a slightly lower, but flexible rate might be better. Platforms like MEXC and Binance offer both options (flexible and fixed).

Security and Compliance: If you prioritize regulated platforms and oversight, lean towards ones like Kraken or even Coinbase (though Coinbase’s USDT support is limited; they focus on USDC). Centralized exchanges generally have more compliance safeguards, whereas smaller or offshore ones might carry more risk.

Liquidity Needs: If you might need funds on short notice, choose platforms with instant withdrawal (TetherYield, MEXC flexible, Binance flexible). If you know you won’t touch it for 3 months, then locking on a high-rate plan could make sense.

Platform Focus: Some platforms specialize in stablecoin yields (TetherYield, and Nexo to an extent), which means their whole service is oriented around that, potentially offering a smoother and more transparent experience for that purpose.

Always remember to do a bit of homework on any platform you entrust with your assets: read reviews, check their security measures, and make sure their offering is legitimate (unrealistically high rates can sometimes be red flags, unless clearly explained how they’re achieved).Next, we’ll delve deeper into TetherYield.com’s offering, since it’s a standout platform for USDT staking, to understand why it can provide such high yields and how it addresses user needs.Step-by-step guide showing how to start staking USDT on TetherYield ConclusionStablecoin staking has truly come into its own by 2025, transforming what used to be idle digital dollars into a dynamic source of income. USDT staking allows investors to earn impressive yields without taking on the wild price volatility of other crypto assets. We’ve explored how it works, why it’s become so popular, and the landscape of platforms competing to offer you the best return on your Tether.For investors who love the stability of cash but crave better returns, staking USDT is a game-changer. Instead of letting your dollars collect dust at near-zero interest, you can convert them to USDT and potentially earn anywhere from a steady 5% to 10% APY on mainstream platforms, up to double or triple-digit APYs on specialized services like TetherYield. That is significant passive income that can help grow your wealth or generate extra cash flow each month.We also compared major options: CeFi providers bring convenience and trust, DeFi protocols bring control and higher base rates, and hybrid platforms like TetherYield bring unrivaled yield with managed risk. The best approach for many may be a mix – keep some funds on a big exchange for accessibility, and allocate some to higher-yield platforms for maximum growth. Always remember the golden rule of investing: diversify and do your due diligence. Even in the relatively stable realm of stablecoin staking, spreading out your risk and choosing reputable, secure platforms is key.To recap a few key takeaways:

USDT staking is an accessible strategy to earn interest on crypto dollars, beneficial for both crypto enthusiasts and traditional investors seeking entry to crypto with lower risk.

It offers consistency and reliability, which, in a volatile market, can be very valuable for balancing a portfolio.

The returns on USDT staking outshine traditional finance – making it attractive in today’s low-interest environment for cash.

There are many platforms to choose from; the top platforms of 2025 include TetherYield, Binance, OKX, MEXC, Kraken, among others, each catering to different needs (extreme yield vs. simplicity vs. regulatory peace of mind).

TetherYield.com emerges as a leader for those prioritizing maximum yield and strong security, essentially unlocking the full earning potential of USDT in a way few others can match.

As with any financial strategy, it’s important to stay informed. The crypto industry evolves quickly – new opportunities and regulations will continue to shape the USDT staking landscape. Keep an eye on interest rate trends, platform announcements, and the health of the stablecoin market. By doing so, you can adjust your strategy to remain both profitable and safe.Finally, if you’re ready to put your USDT to work, consider starting with a platform that aligns with your goals and comfort level. If you value top-tier yields and are impressed by what you’ve learned about TetherYield, it could be a great place to begin or enhance your staking journey. On the other hand, if you’re just dipping your toes, maybe start on an exchange you already use, then graduate to more advanced platforms as you gain confidence.Your USDT doesn’t have to sit idle. Staking can empower you to earn a passive income stream 24/7, even while you sleep – truly letting your money work for you. With the knowledge from this guide, you’re well-equipped to venture into USDT staking strategically and responsibly. Here’s to turning those stablecoins into a stable source of wealth!